Compiled from Freedom of Information requests to local authorities, the index offers one of the most comprehensive snapshots of council solar deployment in the absence of any central government dataset.

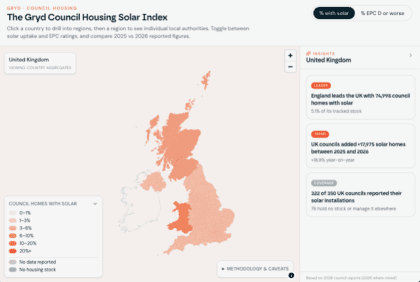

7.8% (1.67 million) of privately owned and tenanted homes now have solar systems installed*, compared with 5.8% (112,865) of council homes nationally. Yet council housing in Wales and Scotland surpasses private homeowners: 10% and 8.6% of their council homes are equipped with solar respectively – demonstrating local authorities’ potential to lead the UK’s transition to clean home energy.

Local authorities in North West Wales lead by a wide margin, with one in three council homes (33.8%) now fitted with solar panels, followed by North East Wales (21.7%) and Scotland’s Aberdeen and North East (13%).

Southern Wales reported the sharpest rise in progress, increasing from just 0.3% of council homes with solar last year – the lowest rate in the UK – to 8.1% today, bringing the region to around the national median. Scotland’s Highlands and Islands also made considerable gains, with rooftop solar now on 9% of council homes compared with 4.7% last year.

In England, the East Midlands stands out as the most improved region, accounting for more than one-third of all new council solar installations nationally over the past year. The number of solar-powered council homes there nearly doubled in twelve months, from 4,875 to 9,625.

At the other end of the scale, London records the lowest proportion of solar-powered council homes at just 1.6%. Low rates are also reported in Edinburgh and Lothians (2.7%), South East Wales (2.8%), South West Wales (2.9%), and Yorkshire and the Humber (3%). Progress across England and Northern Ireland has remained largely static overall, with solar reaching 5.1% and 3.9% of council homes respectively, almost unchanged from the previous year.

“We created this index because there was no clear picture of where the UK stood on solar across council housing,” said Mohamed Gaafar, CEO and Co-Founder of Gryd. “Without that visibility, it’s impossible to measure progress or identify where parts of the country might be getting left behind in the clean energy transition. Social housing tenants are among the most vulnerable to fuel poverty, with the least ability to act independently when costs rise. Tracking where solar is and isn’t reaching them is the first step to closing that gap.

“Councils are frequently more ambitious than private developers in installing larger systems and demonstrating genuine appetite for solar at scale. Wales and Scotland prove that ambition can translate into results, but for many councils the barrier is rarely ambition alone – it’s upfront capital, and how to best allocate what you have available,” says Gaafar.

“Key government funding pathways have closed at a critical moment – the Warm Homes Social Housing Fund is no longer accepting applications, and ECO4 Flex is nearing the end of its available resource. That risks taking significant momentum out of the market.

“The good news is that the government is moving in the right direction. If the upcoming tranche of Warm Homes Fund investment is deployed effectively, we could well see councils leapfrogging the private market by this time next year.

“But councils’ reliance on government funding cycles alone creates stop-start progress. While public funding will always be essential, partnering with private capital can also help councils and housing providers accelerate deployment at a scale that current budgets struggle to support. Private capital has long favoured solar and other renewables, drawn by the maturity of the technology and the certainty and stability of the returns – nearly $1 trillion was invested in solar globally over the last two years alone**. The capital is there; what’s needed is effective policy to let it flow in at pace and scale – ensuring the benefits of the clean energy transition are felt equally across every type of household.”